House Affordability Calculator: Rent or Buy?

A California-focused calculator that finds your maximum affordable home price and compares the wealth outcomes of buying versus renting and investing

TL;DR: Buying a $1.5M house in California and holding for 10 years is financially equivalent to renting at $12k/month. Your actual rent is probably a third of that. The gap is a massive, hidden arbitrage opportunity that most people miss because "$12k/month in rent" sounds obscene. Until you realize buying quietly costs even more. This calculator shows you the math.

The number that changed how I think about housing

Buying a $1.5M house in California is financially equivalent to paying $12k/month in rent.

That number sounds absurd. Nobody would pay $12k/month in rent. But that's the point. When you account for the 20% down payment ($300k in cash tied up and not invested), $7,600/month mortgage payments, property taxes, insurance, maintenance, 8% selling costs, and the 10% annual returns you'd earn investing that cash instead, buying the house costs more than $12k/month in rent over a 10-year hold.

And here's the arbitrage: a $12k/month rental in California gets you a house that is in an entirely different league than what $1.5M buys. We're talking 4,000+ sq ft homes in top neighborhoods, the kind of properties that sell for $3-4M. The renter lives in a nicer home and ends up wealthier.

This is what "equivalent rent" reveals. It strips away the emotional framing and shows the true cost of buying. When your actual rent is $4,500/month and the equivalent rent is $12k, that $7.5k/month gap is real money. Roughly $90,000 per year in wealth you keep by renting and investing the difference.

The number holds up across assumptions. At 8% investment returns, equivalent rent is ~$12.5k. Even if the home appreciates at 5% per year (matching rent growth), it's still above $11k. Push both levers in the buyer's favor (high appreciation, low stock returns) and the equivalent rent still clears $10k/month. The fundamental conclusion doesn't change: buying is far more expensive than it looks.

The rest of this post explains the full methodology, walks through the sensitivity analysis, and gives you a calculator to run your own numbers. But if you take one thing from this page, it's that number: $12k/month. Compare it to what you actually pay in rent. The gap is your arbitrage.

Why I built this

I was recently considering buying a house in California. The decision carries heavy emotional weight, especially given the prices here. I'd used several online calculators that all gave wildly different numbers, and none of them helped me answer the real question: should I even buy at all?

Everyone around me kept saying renting is "throwing money away." Friends and family ask "when are you buying a house?" as if it's an inevitable life milestone. But I wanted to approach this decision pragmatically, without emotions clouding the economics. When I ran the numbers, the answer surprised me. In many scenarios, the renter who invests their down payment and monthly savings builds significantly more wealth than the buyer.

That's what this tool shows you. If you're facing the same decision, the math may change how you think about it.

What's already out there

There's no shortage of rent-vs-buy resources. The NYT Upshot calculator is the gold standard for interactive sliders and tells you a breakeven year. NerdWallet and Zillow offer solid calculators with market data. Khan Academy walks through the economics step by step. Ramit Sethi has been making the case that renting is not throwing money away for years. Of Dollars and Data takes a deliberately simple approach. The Bogleheads wiki compiles the evidence.

But none of them answer the question the way most people actually think about it: I pay rent, I pay a mortgage, which one makes me wealthier over X years? Most calculators either find your affordability ceiling or compare costs, not both. They use a single set of assumptions and give you a single answer. And they don't show you how uncertain that answer is.

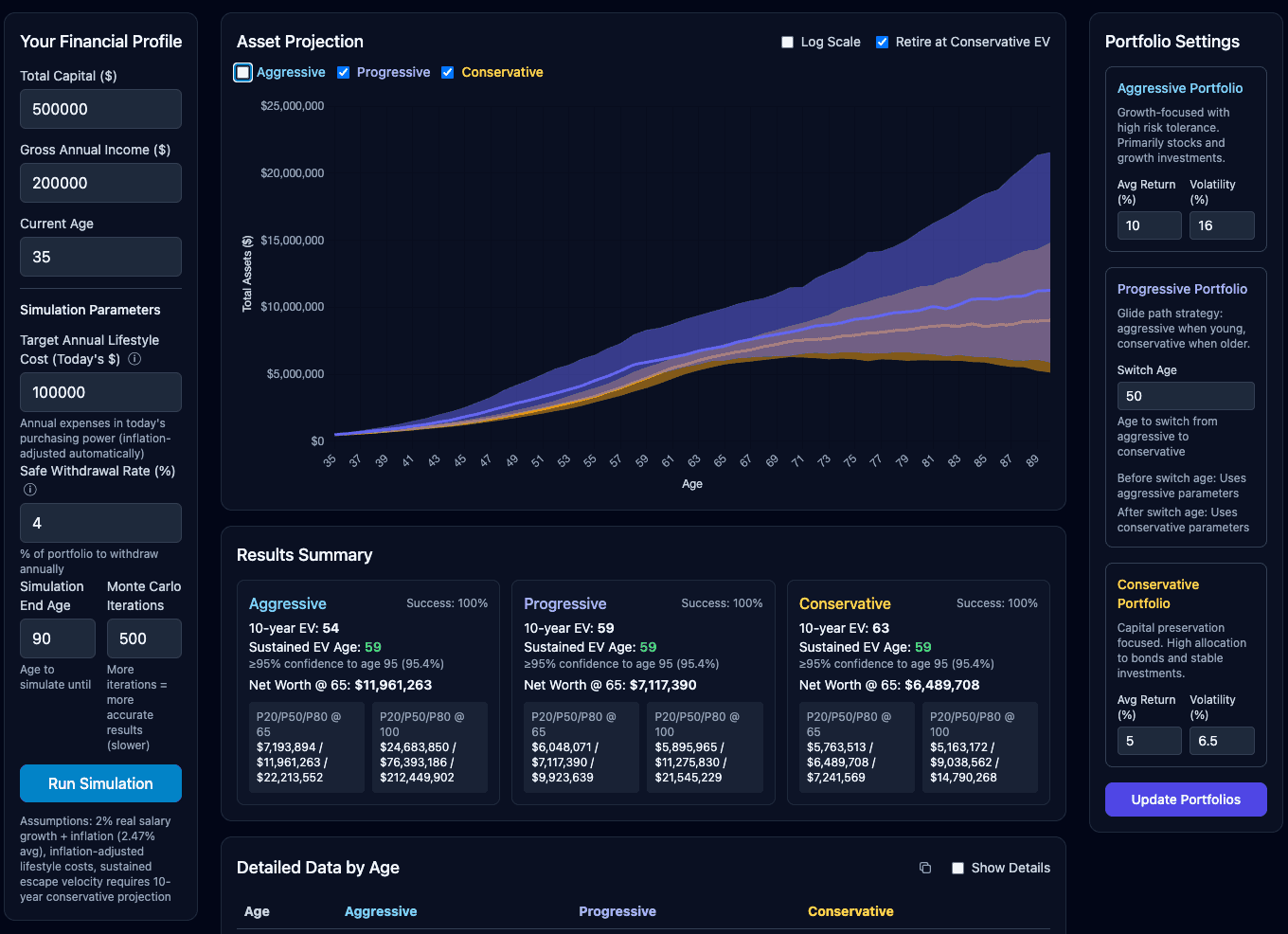

This calculator does all three. It finds the most expensive home you can safely afford, runs a full rent-vs-buy wealth comparison at that price, and uses Monte Carlo simulation to show you the range of outcomes rather than a single guess.

The real question: rent or buy?

Most affordability calculators answer the wrong question. They tell you "how much house can my income support" based on a simple debt-to-income ratio. But the financial question that actually matters is: does the wealth you build through home equity exceed the wealth you'd build by investing the same capital?

Before getting to the math, it's worth acknowledging the emotional biases that cloud this decision:

- Ownership bias: We overvalue things we own. A house feels like "yours" in a way that a portfolio doesn't, even if the portfolio is worth more

- Sunk cost framing: "Rent is throwing money away" ignores that mortgage interest, property tax, insurance, and maintenance are also money you'll never see again

- Social pressure: "When are you buying?" carries an implicit judgment that renting is temporary or inferior

- Loss aversion: Missing out on home price appreciation feels worse than missing out on stock market returns, even if the latter is larger

- Anchoring to monthly payment: Comparing mortgage payment to rent ignores the massive opportunity cost of the down payment

These aren't financial arguments. They're emotional ones. The calculator strips them away and shows you the math.

What the numbers show

The rent-vs-buy comparison reveals several things that conventional wisdom gets wrong:

Take a $1.5M California home: 20% down, 6.5% mortgage, 3% home appreciation, 10% investment returns, and 8% selling costs. Over 10 years, the equivalent rent is $12k/month. If you're paying $4,500/month in actual rent, that's a $7.5k/month gap, roughly $90k/year in wealth you preserve by renting and investing. Run the calculator with your own numbers; the assumptions matter, and that's the whole point.

Equivalent rent: the single metric that matters

Equivalent rent is the monthly rent at which buying and renting produce identical wealth outcomes over your time horizon. If your actual market rent is below this number, renting wins financially. The further below, the stronger the renting advantage.

This one number captures everything: down payment opportunity cost, mortgage interest, property tax, insurance, maintenance, tax benefits, home appreciation, selling costs, and investment returns. You don't need to weigh 12 different factors. Just compare your rent to the equivalent rent.

Investment return assumptions swing the verdict dramatically

The sensitivity table in the calculator shows equivalent rent at different investment return rates (0% to 15%). Higher assumed returns increase the opportunity cost of the down payment, which pushes equivalent rent up. But even at conservative return assumptions, the equivalent rent stays well above typical market rents.

This is why the rent-vs-buy debate is so contentious. People with different investment return assumptions will reach different conclusions. The sensitivity table lets you see exactly where the crossover is for your situation.

Selling costs: the hidden 8% drag

When you sell a home, you lose roughly 8% to agent commissions, transfer taxes, and escrow costs. On a $2M home, that's $160k gone. Most simple calculators ignore this, which dramatically overstates the buying case, especially for shorter hold periods.

Tax benefits: the standard deduction caveat

The "mortgage interest deduction" is one of the most cited benefits of homeownership. But since the 2017 tax reform raised the standard deduction, most buyers get little or no incremental tax benefit. You only save on the portion of mortgage interest plus property tax that exceeds the standard deduction. The calculator estimates this using your marginal tax rate and standard deduction (both configurable), though it uses a simplified model that ignores SALT limits, filing status nuances, and AMT.

Rent growth: 5% is what we're seeing

The calculator defaults to 5% annual rent increases. This reflects what we've consistently seen in the Bay Area, where landlords typically raise rents close to the maximum permitted by law. If you use a lower assumption (say 3.5%), the equivalent rent drops. But in California's rent-controlled markets, 5% is grounded in reality.

Hold period: time is the buyer's best friend

Short holds are almost always financially bad for buyers. Closing costs, selling costs, and the up-front cash deployment don't get enough time to amortize. The calculator lets you toggle between 5, 10, and 30 years to see exactly how time changes the math. Use this to understand how long you'd need to stay to make buying work.

Monthly premium: what you're actually paying to own

The "Monthly Premium" metric shows how much more buying costs per month versus renting, after accounting for principal paydown and tax benefits. In year 1, this premium is typically significant. Over time, it shrinks as rent escalates but your mortgage stays fixed. The crossover point, if it exists, tells you when buying's monthly cost drops below renting's.

The leverage argument

The strongest financial case for buying is leverage. A 20% down payment gives you 5:1 exposure to home price appreciation. If your home appreciates 3%/yr, your equity grows at an effective 15%/yr on the cash invested.

But leverage cuts both ways. A 10% price decline wipes out half your down payment. And unlike a stock portfolio, the carrying costs are relentless: mortgage interest, property tax, insurance, and maintenance all reduce the net return on that leveraged position. The calculator captures this fully in the comparison. When the numbers still favor renting, it means the carrying costs are eating the leverage advantage and then some.

Refinancing: the buyer's optionality

One advantage the calculator doesn't model is refinancing. If you lock in at 6.5% today and rates drop to 4.5% in a few years, you can refinance and significantly reduce your carrying costs. The renter gets no equivalent optionality. In our $1.5M scenario, a refi to 4.5% in year 3 drops the equivalent rent from ~$12k to ~$11.6k. Meaningful, but not enough to change the fundamental picture. The equivalent rent still clears $11k.

How the calculator works

The calculator has two parts. First, it finds the maximum home price you can afford by simulating 1,000 versions of your financial future with varying income growth and inflation, checking that you can sustain the payments without draining your reserves. Second, it runs a detailed rent-vs-buy comparison at that price: month-by-month costs on both sides, investment returns on savings, tax benefits, selling costs, and the equivalent rent that makes the two paths equal. The net worth chart combines both views, showing a range of buying outcomes alongside a renting baseline.

The core logic works for any US market, but the defaults (1.1% property tax with Prop 13 escalation, 0.35% insurance) are calibrated for California. Adjust these in Advanced Settings if you're in another state.

How to use it

-

Enter your financial details and click "Calculate Affordability": Income, liquid assets, current rent, and annual non-housing spending. The simulation runs in about one to two seconds

-

Check the rent-vs-buy comparison: Look at the side-by-side breakdown. Pay special attention to the equivalent rent and how it compares to your actual rent

-

Toggle hold periods: Switch between 5, 10, and 30 years to see how time changes the verdict

-

Study the sensitivity table: See how different investment return assumptions swing the outcome. If renting only wins at very high return assumptions, you can feel more confident about buying

-

Examine the net worth chart and risk analysis: The chart shows how total net worth compares under buying vs. renting over 30 years. The risk analysis breaks down the probability of cash shortfall, reserve depletion, and housing cost burden at your affordable price

Launch the calculator

🏠 Open calculator in full screen →The emotional case for owning

Buying a home can still be the right call. There are real benefits that don't show up in a spreadsheet:

- Stability: No landlord can decide not to renew your lease. No surprise rent increases beyond your control

- Customization: Paint the walls, renovate the kitchen, build the deck. It's yours

- Community: Putting down roots in a neighborhood, knowing your neighbors, feeling settled

- Pride of ownership: The deeply human satisfaction of having a place that's truly yours

- No landlord friction: No maintenance requests that take weeks, no inspections, no restrictions on pets or guests

These are real and valid. But they're a separate ledger from the financial analysis. The right approach is to know the financial cost of the emotional benefit, and then decide whether it's worth it to you.

If renting saves you $500k over 10 years but you value the stability and pride of ownership, that's a legitimate choice. Just make sure you're making it deliberately, not under the illusion that buying is "always the smart financial move."

Emotions, data, and hidden arbitrage

Many of our biggest financial decisions are driven by emotions and preconceived notions rather than data. Getting to the numbers reveals arbitrage opportunities hidden behind conventional wisdom.

Rent-vs-buy is a prime example. In many markets, the renter who invests their savings ends up wealthier than the buyer. But social pressure, the "throwing away money" narrative, and the deeply human desire to own make it nearly impossible to see.

There's one important caveat: the math assumes you actually invest the savings every month rather than spending them. A home is a forced savings vehicle. Every mortgage payment builds equity whether you're disciplined or not. The renting advantage only materializes if you consistently invest the difference. For many people, that discipline is the hard part, and it's where the theoretical advantage breaks down in practice. If you know you'd spend the savings, buying may be the better path precisely because it removes the choice.

The calculator strips away the emotion and shows you the math. What you do with that information is up to you, but make sure the choice is yours, not a reflex.

Important disclaimer

This calculator is for educational and planning purposes only. It is not financial, tax, or legal advice. The projections are based on assumptions that may not reflect your actual situation or future market conditions.

Key limitations:

- Tax estimates are simplified: The Monte Carlo affordability engine uses a rough 70% take-home approximation. The rent-vs-buy comparison uses a marginal tax rate on excess deductions over the standard deduction with SALT cap ($10k), but ignores filing status nuances and AMT

- Selling costs are approximate: The default 8% covers agent commission, transfer tax, and escrow, but actual costs vary by location and negotiation

- Insurance availability: California's insurance market is challenging. Getting coverage at any price may be difficult in some areas

- Market conditions: Property values, interest rates, and inflation are unpredictable

- The rent-vs-buy comparison is deterministic: It uses a more granular cost model than the Monte Carlo engine (Prop 13 with 2%/yr cap for property tax, inflation-based insurance, home-value-based maintenance) but does not include income volatility or stochastic modeling

- Different cost inflation models: The Monte Carlo engine inflates all non-mortgage costs uniformly for simulation speed. The deterministic comparison uses per-item inflation (Prop 13 for tax, general inflation for insurance, home-value tracking for maintenance). Results may differ slightly

- Renting scenario uses mean assumptions: The renting line in the net worth chart uses deterministic mean assumptions (no Monte Carlo) and should be treated as directional, not precise

Always consult with qualified financial advisors, mortgage professionals, and real estate agents before making purchasing decisions.

Technical notes

The calculator runs entirely in your browser using JavaScript Web Workers. No personal data is transmitted to any server. All calculations happen locally on your device.

The source code implements:

- Standard mortgage amortization formulas

- Box-Muller transform for normally distributed random variables

- Binary search for optimal price finding

- Deterministic rent-vs-buy comparison with Prop 13 property tax model, inflation-based insurance, home-value-based maintenance, marginal tax benefit on excess deductions, selling costs, and equivalent rent calculation

- Chart.js for visualizations

Questions or feedback?

If you have questions about the calculator or suggestions for improvements, please reach out.

Get more frameworks like this

Practical AI strategy for executives. No hype, just real playbooks.

SubscribeYou might also like